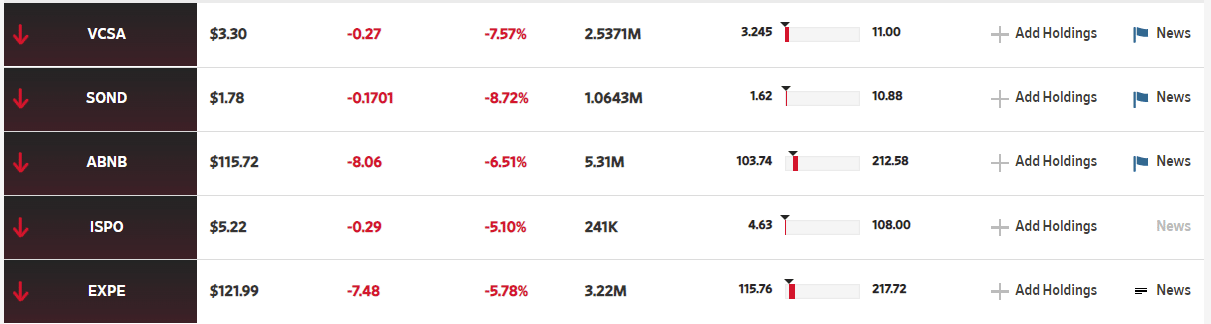

Since Monday, Vacasa (NASDAQ: VCSA) stock has fallen over 30 percent as trading volume increased and lock-up restrictions expired. The stock had a trading volume of 2,536,505 shares, compared to its average volume of 915,445.

1:38 ET: Updated Jun 10 to reflect accurate number of shares held by Eric Breon (65,242,864), and Goldman Sachs target at $5.50 instead of $6.50.

Since its IPO, Vacasa stock is down over 67 percent, closing on Thursday at $3.30.

On Thursday, Vacasa had its price target reduced by equities research analysts at JMP Securities from $12.00 to $6.50, and Goldman Sachs dropped it from $9.00 to $5.50. Zacks Investment Research cut Vacasa from a “hold” rating to a “sell” rating in a report on Tuesday.

The chart below compares performance at Vacasa, Sonder, and Airbnb over the last 90 days.

Low Float

Some analysts are attributing the volatility to the low float. Corporate insiders own 37 percent, and hedge funds and other institutional investors own 36.21 percent of the company’s stock.

On the day of Vacasa’s IPO, CEO Matt Roberts warned of volatility in an interview with VRM Intel. “There’s going to be—over X period of time—there’s a lot of volatility,” Roberts said. “There’s not a lot of float in the market. So any move in the stock, that’s going to be exaggerated. And when it’s super high, guess what, we’re not brilliant and awesome. And when it goes down a lot, it doesn’t mean we did something wrong either. It’s just volatility. So hopefully they can take that message and take it to heart. There’s this human nature to want to look at it—and I understand that and I appreciate that—but I really want them to focus on delivering great service, and then everything will take care of itself.”

SPACS Are Underperforming across the Board

The two highest-profile SPACS in the short-term rental industry, Sonder and Vacasa, have fallen sharply since their IPOs with Sonder down 82 percentand Vacasa down 67.5 percent since their NASDAQ debuts.

Today, Sonder announced in an internal memo that it has laid off 21 percent of its employees and will carry out this layoff over the next two weeks.

The chart below compares performance at market close on Thursday, June 9.

According to Dot.LA—as a refresher—a SPAC is a financial mechanism that allows a company to circumvent many of the regulatory hurdles involved in a traditional IPO as it goes public. The speed of the process made it popular in the tech sector. The SPAC model begins when a shell company (with no assets or business of its own, really) goes public through an IPO. Because the company is only a shell, the IPO process is extremely simplified with far fewer SEC hoops to jump through. Investors in the shell company typically receive stock at $10 per share as well as warrants, which are additional securities that allow them to purchase discounted stock in the future. The shell company then goes hunting for a promising startup that wants to go public.

SPACs aren’t performing well.

“While the stock market at large has certainly been bearish recently, the Defiance Next Gen SPAC Derived ETF (SPAK)—a fund that tracks a huge swath of SPAC performance—has declined around 30% since the start of the year, far outstripping the decline of the S&P 500 (which is down around 13% in that time). Add in a smattering of high-profile catastrophes like WeWork, and the space has started to look like a losing proposition to many investors.”

SPACS are also facing heightened scrutiny from regulators. At the end of May, the SEC proposed tighter restrictions on the SPAC market that are designed to protect investors. The SPAC strategy has been accused by critics of offering outrageous value to the sponsors who initially form the shell companies, while offloading much of the risk onto retail investors. The SEC’s proposed regulations aim to rebalance the scales and provide increased transparency—which, for sponsors, makes starting a new SPAC less attractive.

However, although low float and underwhelming SPAC performance are factors, they don’t tell the whole story of what is going on at Sonder and Vacasa. Industry experts point to inflated valuations as the leading contributor as these companies misidentified themselves as SaaS-based technology companies.

It is possible we will see Vacasa follow Sonder’s lead with financial restructuring and layoffs if its market performance approaches the losses the industry is currently seeing at Sonder.

There has been a recent whirlwind of acquisition activity in the vacation rental industry as national brands look to rapidly grow their portfolios. Although the industry has had a consistent increase in the number of vacation rental management companies selling over the last three years, what makes 2022’s acquisitions unique is who is selling as many of the companies below were founded by some of the industry’s most widely known thought leaders, including VRMA board presidents, regional association board members, former destination CVB and chamber presidents, podcasters, and popular conference speakers.

According to a Vacasa spokesperson, “What I can share regarding 2022 deals is that Vacasa added seven new portfolios during the first quarter . . . We can’t announce names of companies that haven’t been officially disclosed yet.”

Yet, here’s what we know from other sources . . .

Seachange Vacation Rentals: Rehoboth Beach, Delaware

Concept Ux User Experience Development Design Usability Improve software develop company. UI Interface experiment design improve Vector illustration project guide build Web app Computer, responsive.

Vacation rental managers have a lot on their plates. Outdated website content and overall “website cleanliness” is often something VRMs know they need to address, but there’s a long list of more important items above that on their to-do list. And once some of those more important items get crossed off, more just end up arising that take their place.

This results in websites and blogs that have become cluttered over time with information that is no longer relevant, links to properties that aren’t in inventories anymore, resource links to local businesses that are no longer in business, outdated policies, spammy pages that were created to try to manipulate search engines back in the day, and a long list of other possible issues that need to be taken care of.

This not only makes for a poor user experience, but it can negatively impact SEO, which hurts your overall bookings and revenue. If you know you’ve been neglecting your site for a while, then I highly recommend taking some time to give it a thorough cleaning.

If you can’t find the time or want to ensure it’s done properly, you can always hire an SEO company to take care of it for you. But if you’re ready to take this on yourself or with your in-house team, here is how I would go about doing it.

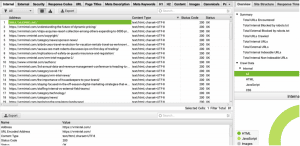

Run a site crawl

Before we get into the five steps, there are two things I highly recommend doing before you get started. The first is to run a site crawl. This isn’t crucial, but it certainly makes things easier. Depending on which crawler you use, you can get an overview of every URL on your site which you can then break out into an organized spreadsheet. I recommend a software called Screaming Frog for this, but there are several that will do the job.

This will not only give you a list of every page that is linked to on your site but will give you any URLs with 404 status codes that were returned, which you’ll need for later in the cleanup process.

Backup your site

And for safekeeping, you always want to ensure you have a backup of your website before you start overhauling your content. The last thing you want to happen is to see your traffic start to drop because you deleted something you shouldn’t have and not have any way to restore it.

Once that’s out of the way, you can get into the actual cleanup process.

1. Organize Your CMS

One thing we’ve seen many clients guilty of is letting old, unused pages pile up in the admin of their website. Cleaning this up generally doesn’t take long and will make things easier on you and anybody else working on your website.

Go through all of the pages in your content management system (CMS) and delete any that don’t get used. It’s important that you actually go through your admin and check these pages instead of looking through the site crawl for these. The site crawl only picks up pages that are linked to somewhere on the site, so oftentimes, the pages that need to be deleted from the CMS aren’t in the site crawl.

This includes pages like test pages, draft pages that were started but never finished, duplicate pages, the 2019 Labor Day weekend special page that was made to use in an e-blast, etc.

Having a clean CMS will make it easier on your team to find pages in your admin. On top of that, if your site automatically adds all pages to your sitemap, then Google is crawling all of these pages, and it can have a negative impact on SEO if your sitemap is full of test and draft pages using Lorem Ipsum text.

2. Clean Up Your Blog

Outdated content is far more common on blogs than on website pages. We’ve seen blogs in this industry with 1,000+ blog posts dating back to the 2000s. As daunting of a task as it might seem to have to clean up a blog like this and as much as you might be tempted to skip this step if you have a ton of blog content, there are quite a few reasons it’s worth taking the time to do. Here are just a few:

• To avoid a lawsuit

One of the most important reasons to clean your blog is to protect yourself from copyright infringements on old images. You may think you’ll never get sued for that, but I assure you it happens.

If you know for certain that you’ve only used images that you or someone on your team took yourselves or stock images that you had the rights to use, then you’re safe. If you’re not sure about this though, which is often the case when there’s been a handful of staff members or freelance writers posting on your blog over the years, then it’s important to check all of the images on your posts and make sure they’re either your images or if they’re stock images, that they’re properly attributed if their stock licensing requires it.

• To prevent inaccurate information about the area

Another important reason to clean your blog is to avoid misleading people. Outdated information anywhere on your site can be misleading, but in the case of blogs, the outdated information often doesn’t just pertain to your company. If you have old posts that were written to be area guides for your guests then you likely have a good deal of outdated information out there about events or local businesses in your area.

There are plenty of reasons this can be problematic, but one fairly common example I’ve seen of this is when vacation rental companies publish posts about nearby annual events. The post gets published prior to the event and then forgotten about once the event is over. Then over time, the post makes its way up Google’s rankings. The post failed to mention the year because the author assumed it was implied that it was the same year it was posted. What you end up with is a post with a month, day, and time that ranks high on Google for the event name but has an old date, and then that post confuses the users who click it into thinking that’s the upcoming date for the years to come.

• To preserve crawl budget

Google’s bots are constantly crawling websites. Google sets a crawl budget so that its bots don’t get hung up on crawling every page of the massive sites that are out there and instead stop and move on to the next one. This crawl budget results in many sites not getting fully crawled when the Googlebot stops by.

By eliminating outdated blog posts, you’re limiting wasteful crawling and ensuring your important pages and up-to-date posts are getting crawled regularly.

This also applies to tags and category pages created in WordPress. It might be the case that you only have 50 published blog posts, but you have 1,000 blog tags that someone on your team created mistakenly thinking they would help SEO. The pages WordPress creates for each of those tags are just as capable of wasting a crawl budget as the outdated blog posts.

How to actually clean your blog – Your response to everything you just read might be to just delete everything on your blog more than a year old, but please don’t let that be the takeaway.

Take the time to assess how the blog posts are performing using Analytics and Search Console. You don’t want to delete posts that are getting clicks and suddenly see your traffic tank. You’d be surprised how many sites have an old random blog post bringing more traffic to the site than any of its main site pages.

Anything that hasn’t gotten at least ten clicks in the past two years is probably fine to get rid of. That’s hard to say definitively without actually seeing what the post is, but that’s a general rule I would go by. If a post isn’t doing well but you feel it’s a quality post that is still relevant, you can always delete it, revamp it, and post it again. If you have multiple posts about a similar topic, you can combine the lesser performing ones with the best performing one, and then delete the lesser ones. Just remember to redirect those URLs to the one you’re keeping.

There’s a lot that can be done to ensure this is done correctly and in a way that benefits SEO instead of negatively impacting it. If you don’t have someone on your team that is well-equipped to do this, then I would recommend hiring an SEO company for it.

3. Update Outdated Content on Site Pages

Outdated content on your site pages is generally more often seen than outdated content on your blog, but you’re less likely to have as much. This includes your homepage, your property pages, the pages in your navigation, and any internal content pages being linked to from within those pages.

Common issues here can be things like outdated staff bios, no longer applicable policies or FAQ answers, old office hours, outdated information about resorts, numbers that are no longer accurate (ex: “150+ properties” when there are now only 146), and having a previous year in the footer’s copyright notice.

Finding and updating outdated content on your site pages is fairly straightforward work, so you can assign this out to reservationists or other employees when they’re not busy.

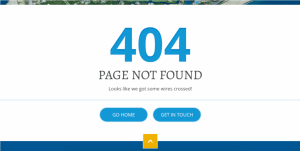

4. Resolve 404s

Your site crawl should have provided you a list of every page being linked to your site that is returning a 404 status code. Each of these 404s means you either have a faulty link somewhere on the site or the page the link was originally pointing to no longer exists.

The ideal way to handle these 404s is to identify where the link is that is creating the 404 and then decide whether the link needs to be removed or whether the page should actually be there. Most crawlers will give you the referring URL so you know which page the broken link is on. If the 404ing page should exist, then check in the CMS and investigate why it’s not. It could be that the page was accidentally deleted or it could be that the page still exists but someone changed its slug. It’s also common to see 404s for old properties that are no longer in your inventory.

If the slug changed and the page had SEO weight, then you need to redirect the old URL to the new one to try to preserve the authority that was lost when the slug was changed and the old URL wasn’t redirected. Putting redirects in is crucial if you’re changing slugs, but I wouldn’t use them as a band-aid to resolve all of your 404s. They can quickly fix them, but they can end up creating redirect chains over time and result in more clutter and disorganization. That brings me to my next point.

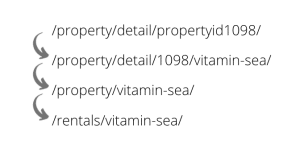

5. Eliminate Redirect Chains

Redirect chains are essentially redirects to other redirects. This is common when a company has undergone multiple new site developments in the past. Each time a new site launches (unless the slugs stayed exactly the same) the old slugs should have been redirected to the new ones.

You also might have marketing teams and in-house staff changing slugs and redirecting them during the time the sites are live so you end up with chains of redirects that could look something like this:

The ideal scenario and best SEO practice is to have all of the previous property URLs go straight to the current URL instead of creating these chains. Redirect chains make it harder for Google to crawl your site, and with enough of them, you can hurt your site speed.

Hopefully, after reading this, you’re motivated to make this the year you give your website the likely long overdue cleaning it needs. If you follow these steps, you’ll end up with a more organized and resourceful website that is performing better in search results. Cleaning your site might seem tedious, but it can ultimately result in more traffic, more money, and fewer headaches in the future.

VTrips announced the recent acquisition of four vacation rental management companies, expanding its portfolio throughout the United States to 7,000 properties and 1,000 employees.

Mike Harrington, founder of Carolina Retreats and former president of the Vacation Rental Management Association (VRMA), offered the following statement to the company’s property owners: “As of June 1, Carolina Retreats has partnered with VTrips Holdings, a Florida-based vacation rental management company led by my good friend, Steve Milo. Steve, Stuart (Pack, vice president and COO for Carolina Retreats), and I go back over a decade when Steve was an early mentor of mine as I was getting started in the vacation rental management industry. We served on the board of the Vacation Rental Management Association (VRMA) together, where Steve was instrumental in helping me bring back innovative ideas to help improve our homeowners’ revenue and property care and delight our guests.”

Harrington will maintain full ownership of his hospitality investment businesses.

According to VTrips founder and CEO Steve Milo, VTrips offered positions at the same or better pay and benefits to all employees of Carolina Retreats, Tybee Vacation Rentals, Silver Sands and Miss Kitty’s Fishing Getaways.

“VTrips believes that employees are the lifeblood of these companies, and we are doing everything possible to create a positive environment for them. As certain large national buyers operate more like ‘strip miners’ in our industry, we are encountering more and more sellers who want a buyer that will hire all their staff, take care of their brand and legacy, and allow them to live proudly in their community,” Milo said.

According to Milo, the recent acquisitions were made from the company’s operating profits and commercial bank debt. “Profitability matters, and VTrips continues to be the #1 leader of national vacation rental companies for EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization), compounded EBITDA growth year over year, and EBITDA margin to revenue.”

Ben Edwards of Weatherby Consulting advised Carolina Retreats, Tybee Vacation Rentals and Silver Sands on the sale of the companies. “Having Ben and the team at Weatherby Consulting involved ensures a professional process and that a deal can be moved at lightning speed,” Milo said. “We also know Ben and his team have personally vetted the companies, making them more attractive.”

Jacobie Olin, RSPS, president of C2G Advisors represented Miss Kitty’s Fishing Getaways during the acquisition. “It was a pleasure representing Dawn Huff at Miss Kitty’s Fishing Getaways through the acquisition. She has built a strong brand in Rockport, and we’re happy to see VTrips lead the company into the future. It was a seamless and professional process working with the VTrips team throughout the transaction,” Olin said.

“We tell sellers that certain large national buyers are an option if they intend to move to another state or country and change their cell phone. Some sellers think this is funny. I always have a lot of good stories to share when I meet sellers in person,” Milo added. “Most sellers dedicated their lives to building a legacy and making great memories for their guests and employees, and they want a buyer who shares their same values.”

Milo said that VTrips is well positioned to compete for the industry lead in the resort vacation rental market in North America.

“As a company headquartered in business-friendly Florida, with a founder and owner still in charge and who supports the industry in advocacy and volunteer work, VTrips is positioned to rapidly expand while other large companies deal with leadership and stock turmoil,” he said. Milo also serves as chairperson of the Florida Professional Vacation Rental Coalition, which raised more than $250,000 over the past two years. He is also a member of the VRMA Advocacy Committee, which has so far raised more than $470,000 in 2022.

“Some companies and CEOs care passionately about the future of the industry, and some are just industry outsiders concerned about getting a quick exit from this industry before their operational issues implode on them,” Milo said, adding that the once sleepy vacation rental industry is rapidly transforming. “With these changes, some vacation rental owners are deciding to take chips off the table, and the company they choose to sell to may be the #1 factor.”

Examining how VRM’s can get the most return for their investment in growth

Warning. Spoilers ahead.

In 2001, Billy Beane, the GM of the Oakland Athletics baseball team, was faced with a big problem. His team had just lost to the Yankees in the playoffs, and Beane was losing his three best players to teams that could pay them more money.

You see, The A’s had a payroll of $41 million. The Yankees, $125 million.

How could Beane rebuild his team while competing with organizations that had double or even triple the money to spend?

He knew he had to think differently to win, so he developed a new system of evaluating players to get the most bang for his buck.

Despite a rough start, upsetting his entire organization and nearly losing his job, Beane’s smart, data-driven decisions brought his team back to the playoffs the very next year. And, in the course of doing so, he forever changed the game of baseball.

Now that I’ve ruined the plot of the movie “Moneyball” for all of you who haven’t seen it, I’m going to tell you what it means for vacation rental managers.

Winning through smarter investments

As a business, the decision of where to invest your time, resources and money is one of the primary factors that separates winning companies from losing companies.

The goal behind any investment in your business is almost always to grow your profitability over the long term. This breaks down to either growing your revenue or reducing your costs.

Most vacation rental managers are like the Oakland Athletics. They have small budgets and are trying to compete with the New York Yankees and Boston Red Sox of the industry.

To win, they have to make smart decisions about where to spend their money.

The One Metric that Matters

In baseball, organizations traditionally looked at buying talent. Beane flipped that on its head and instead looked at buying runs, and boiled it down further to the single metric that mattered: getting people on base.

So, what’s the equivalent of “getting on base” in our industry? What’s the one thing that is at the root of how much revenue and profit your business can generate?

I argue it’s the quantity and quality of your homes.

In the vacation rental industry, we sell time in homes. But, each home only has so much time available each year. You can try to maximize your time sold (get more bookings) or increase the price of that time (revenue management). But, at the end of the day, both of those options have upper limits.

The only way to truly grow your revenue at scale is to add new properties. And the mega managers know it. Just look at the growth strategies of Vacasa and Evolve.

Disrupting the Old Belief Systems

For the traditional VRM, growing inventory has always somehow taken a back seat to getting more bookings, revenue management and even operations. You’ll see it reflected by the number of listings sites, revenue management companies and even property management softwares.

For me, this mindset is rooted in two primary beliefs:

Growing your inventory is complicated

The ROI is hard to calculate

However, forward-thinking VRMs are now challenging these beliefs. And reaping the benefits.

Running the Numbers

Let’s examine the return on investment of growing your inventory, using some industry averages.

The average vacation home does about $35,000 in gross booking revenue (GBR) annually.

The average profit a VRM sees for a home is about 10% of the GBR.

And, the average lifetime of a vacation rental contract is about 10 years (based on the average churn rate of 10%).

That works out to a lifetime value of about $35,000 over 10 years, with $3,500 profit annually.

If it takes you one year to recover the cost of acquiring the property, then you start seeing profits in years 2-10.

Benchmarking that against a strong stock market performance of 15%, you can see just how outstanding the ROI of inventory growth really is over the long term (see graph).

Hiring a “Moneyball” General Manager

After Billy Beane pulled off his magic season for the Oakland A’s, the Boston Red Sox offered him the largest contract ever awarded to a general manager (in any sport).

But, Beane turned them down to stay in his small market.

At Vintory, we’ve worked out a system to help VRMs grow their inventory. But, we don’t want to be the GM for the Yankees or the Red Sox.

We want to help level the playing field for independent VRMs.

So, if you’re ready to start playing Moneyball, give us an at bat.

I must admit, sometimes I indulge myself in stock trading. One thing I’ve learned is I’m never going to sell a stock at its highest point; however, it’s always good practice to sell when it’s trending up, as opposed to watching it peak, then reverse.

Right now, the short-term vacation rental market is 🔥. There are more buyers and more money than ever before. A few years ago, sometimes it took several months to receive an offer on your company. Today, we are seeing multiple offers in just a few days. While the buyer demand is certainly there, vacation rental operators will need to contemplate a few things before they decide to sell.

📈 Up and to the Right

For many vacation rental company owners, 2021 was their best financial year since they’ve been established. From inflated daily rates to pent-up guest demand, it’s definitely been a lucrative last twelve months.

Coming out of the strongest financial year to date, many sellers have the opportunity to leverage a multiple of their 2021 EBITDA to receive a high offer. Sounds great, right? Although we’ve seen this happen several times so far in 2022, not every seller is able to cash out at the highest point. There are many established industry buyers and several new ones entering the market; however, they are well versed in mergers & acquisitions and are expecting professional companies. For a seller to get the highest purchase price and terms, they also need to show a strong overall business that’s trending “up and to the right”. Read more about that in Part 1 and Part 2 of our “Prepare Your Company To Sell” series.

💰 Types of Buyers

The amount of interest in the short-term vacation rental industry is at an all-time high. We’re seeing several types of buyers and each one looks at different company metrics, including EBITDA, Net Revenue, and Price per Unit. Read more about buyer metrics here.

>Venture capital-backed: Focused on net revenue, price per unit, and EBITDA >Private equity/family offices: Focused on EBITDA over $1M and over 100 units >Strategic operators: Companies in complementary markets or market competitors looking to expand for cash flow & diversity. Focused on EBITDA

🌼 Season

Most vacation rental markets have seasonality, and peak season is when operating accounts are overflowing. There are pros and cons to consider when selling pre-season and post-season.

Pre-Season

Pro: Typically buyers will put a higher price and less contingencies on the deal structure, for two reasons:

Buyers get to retain the profits from peak season and come into season with a padded trust account

Homeowners are less likely to leave the program when they have a full calendar of bookings

Con: The seller doesn’t get to keep the profits from the season. Also, it can be difficult to manage your company selling while preparing the business for the peak season.

Post-Season (the pros and cons are basically reversed)

Pro: The seller gets to retain the profits from peak season. Con: Typically buyers will place more contingencies when closing after peak season because that is the time when homeowners consider leaving the program. Less bookings = less sticky homeowner contracts.

It’s not easy to decide when and how to sell your business. We can’t predict the future, but we do know the market is hot right now. Having completed transactions from $50K to $220M, C2G Advisors is the “Go-To” company for any size deal. Whether you’re looking to sell your company, strategically merge with another, acquire a company, or need a business valuation, we have the experience and expertise to ensure success.

There is a military adage that states ‘maneuver without firepower is perilous and firepower without maneuver is pointless.’ Without getting into the subtleties of martial arts and science, the concept is that effort, intention, and resources must come together within the context of a strategy to create success. In the vacation rental management business, we call this coordinating and integrating the front of the house with the back of the house.

Get the Back of the House in Order

Buildings are complex structures. Structural integrity, energy usage, access control, and interior comfort are the result of the program manager knowing what is going on at the property. Since no one can be everywhere at once or have the eyes, ears, and nose to know what is always happening, savvy managers use technology to keep a constant watch. Cameras, sensors, detectors, and other devices can be linked to a property control software system to provide real-time updates into the status of every unit in the portfolio.

But data alone gives an incomplete picture. Adopting another military concept, intelligence is produced by combining information with insight. A modern property management platform will tell you what is going on with the buildings in the context of the operating business. The integration of property updates with operating workflows is what creates efficiency. For example, the fact that unit 407’s air conditioner is blowing hard at 62°F is curious. The Smith family checked out two days ago and no one will be accessing the unit until the plumber completes his work order later this week, so why not automate a more eco-friendly temperature while the unit is vacant to save energy, money, and wear and tear?

Operating Processes

In many vacation rental businesses, critical functions like maintenance, front desk, housekeeping, and inspections are managed in isolation as independent silos. Even when theoretically integrated with the use of paper trails and quick updates via phone, text, or email, the right hand usually has little idea as to what the left is doing. If a family decides to extend their stay by one day, how will housekeeping, maintenance, inspections, and even the incoming guest stay informed? A good, unified property management system will automatically update every single interested person and function to make sure that efficiency is gained, and frustrating mishaps are avoided.

Front of the House

When a guest arrives at your property, they want the vacation to begin immediately. Like an iPhone or Android device, that ‘just works,’ without exposing its interior complexity, your property experience needs to operate flawlessly from the guest’s perspective. If your property management platform is properly chosen and configured, it will take the reservation stay information directly from the CRM or third party (e.g. Expedia, Airbnb, VRBO) so there is no risk of transcription errors by retyping.

From the initial point of the booking all the way through departure, a great guest experience will only occur if every department is not only focused but in total sync. Leveraging an enterprise-level unified operations platform such as BeHome247 is the answer to delivering high-quality guest experiences. The alternative is bolting on yet another single-point software solution that is unlikely to add and may indeed detract from efficiency.

Communication Pulls it All Together

Now that the building itself is integrated and operating in sync with the operating workflows of the business, the last piece is to ensure that the guest is kept well informed. Guest experience communication functionality must seamlessly blend with the property control and operations software so guests can best enjoy their vacations with a minimum of human problem solving from your staff.

Before check-in, guests should be reached by email and text to review check-in times, access codes, billing information, and local area information. Further, why not surprise and delight the guest by offering a discounted rate to arrive early or stay an extra night or two, allowing you pack the owner’s calendar and provide a unique value proposition to the guest? Likewise, a guest that has arrived before the stated check-in time can be delighted by an earlier-than-expected unit availability because housekeeping prioritized that space because of being informed.

Conclusion

Like many critical concepts, the building blocks of vacation rental operations excellence are simple to understand and challenging to implement. A modern unified property management platform like BeHome247 gives the property manager the ability to have complete control and visibility over day-to-day operations and communicate effectively with staff and guests alike. Today’s technology allows vacation rental leaders to focus their skills on what they do best by delighting vacations with properties that are pristine and operations that are flawless.

In 2022, consumer demand for vacation rentals is predicted to increase by 14 percent. Additionally, vacation rental inventory is expected to increase by 15 percent (Airdna). The success of our industry is bringing new players to the table, increasing competition, and making it harder — and more crucial — for your brand to stand out from the crowd.

Although findings vary widely regarding the average number of online touchpoints a traveler goes through on their way to purchasing accommodations — results range from 45 to 225 — those interactions offer a wealth of opportunities to put your brand in front of potential guests. To help you capture attention in a saturated market, the Bluetent team has four simple tips designed to put your brand in front of travelers during their journey to the “book now” button.

1. Be the Ultimate Resource for the Information Travelers Need

This isn’t a new suggestion, but it’s an important one and worth mentioning again. With 53.3% of all website traffic coming from organic search (BrightEdge), investing ongoing effort into creating quality website content is essential. Providing relevant content to travelers in the planning stage brings more guests into your booking funnel, and Google rewards purposeful with better positioning in organic search results.

No one knows better than you what your potential guests are looking for, so use your local expertise to build out web pages and blog posts that address your area’s most popular and unique features. Don’t forget to create content for visitors of all ages, kids included. Whether toddler or tween, it’s important to address the needs of all your potential guests: you might gain a lifelong customer in the process.

2. Increase Your Website’s Video Content

Remember that quality content is more than just words and photos, it’s video, too. When you add a video to your home page and landing pages, you can increase conversion rates by more than 80 percent (HubSpot).

Advances in technology have made creating video content possible for almost everybody. In fact, most modern cameras (including those on smartphones) are sufficient for basic video capture. With the addition of a few simple tools — things like a tripod, a microphone, and video editing software — you can develop in-house video content for your brand.

Video brings your brand to life and builds trust with your potential guests: 90 percent of internet searchers report that video content helps them make purchase decisions (Deposit Photos). With that in mind, consider all the potential videos you can create. Go beyond a home page video and start creating property walk-throughs, customer testimonials, and area guides.

3. Pump Up Your Public Reviews

95 percent of travelers read online reviews before deciding to book accommodations (TrustYou) and those reviews can increase conversions by 270 percent (Speigel Research Center). To put it simply: reviews matter!

The old adage, “you don’t get what you don’t ask for” rings true here. We recommend that, after their stay, you ask your guests for reviews. You can make it as simple as clicking a button: send an automated post-departure email containing a link for submitting a review to your Google My Business page.

The information you’ll glean is invaluable to travelers researching a vacation, to the success of your business, and to the satisfaction of your homeowners. Bonus: guests know you’re invested in the quality of their experience.

4. Double Down on Social Media

The reach of social media is undeniable — as of October 2021, the number of social media users worldwide topped 4.55 billion, and that total is increasing by more than a million new users daily (Datareportal) — and also rapidly evolving. Just as video content shared via TikTok and Instagram Reels has already reshaped the music industry, you can expect social media to continue influencing industries across the board. Staying aware of trends and taking the time to post regularly on your social media channels will keep you in the game and in front of travelers.

While boosting your brand’s visibility through social media posts is a good start, don’t forget about the power and reach of social media advertising. By using data about your website visitors and past guests, you can serve the right Facebook and Instagram ads to the right people at just the right time.

We hope these tips have given you a few ideas for getting your brand in front of travelers as they plan their vacations. The experts of Team Bluetent have more tips to share! Reach out at bluetent.com/connect-with-us/.

If you were to reduce your participation in your company by 50%, could your management team successfully run the business? What if you were unable to run your business indefinitely?

These questions are key in evaluating the effectiveness of your management team as operators of the company. Why is this important? Business owners rely on key managers to enact the company’s mission successfully. This can involve including managers in setting strategy, executing the strategy through the division of labor, and coordinating to accomplish key tasks.

Clearly separating the owner and operator roles in your business reduces conflicting priorities and improves your transition options. By having a strong management team in place, as well as a plan to handle any disruptions in management, your management team can be the primary “operator” of your company, thus enhancing your company’s value and expanding your options for potential business transitions in the future.

The first step: Creating a framework to assess your organization

In order to begin mapping over operator responsibilities to your management team, it helps to start with a general management framework.

Owners and management should segment the overall corporate strategy into tasks that are handled by specific roles or groups.

Coordination among key roles should be developed to allow management to work together to achieve common goals. A structure is needed to define the levels of authority and the flow of information between roles. Typically, most companies adopt functional divisions (for example, sales, finance, manufacturing, etc.), where the heads of each function work together to set corporate policy.

Oversight of the divisions is facilitated with systems to monitor company health and enable operations. Systems are important for measuring performance in order to tie managers to specific goals.

The management team sets the tone for the culture of the company. Their management style and establishment of a shared outlook can impact how individuals work with each other and with customers.

Going through this exercise can also highlight any gaps in the existing structure, such as the need to augment management (for example, hiring a CFO) or adjust responsibilities held by current positions. Creating contingency plans can help address potential disruptions due to the departure or retirement of a key leader. Incentive compensation planning and succession planning are two key tools to begin addressing these issues.

Are you using incentive planning to retain and attract talent?

Incentive planning for the closely held business can answer key questions:

Does the current compensation plan appropriately incentivize managers toward achieving company objectives?

Does the current compensation package attract, reward, and retain key employees?

Benchmarking the company’s compensation plan on a regular basis versus those of the industry or geography can identify shortcomings and help attract top talent.

How are you developing resiliency through succession planning?

When a key executive leaves, the company may face numerous risks, including the loss of specialized expertise, a disruption in customer/vendor relationships, and a decrease in employee morale. Succession planning helps minimizes the company’s risk exposure by reducing attrition and ensuring business continuity.

Start the planning process by identifying those positions of key importance. Understanding the requirements of the position and the characteristics needed to be successful can help develop a profile of the role. Based on the profile, interim leaders from other positions within the organization can be identified. If there are gaps in knowledge that must be overcome, the creation of a development plan to prepare successors should be created. Regularly updating the succession plan can keep the company prepared for any surprises.

Ways to enhance the value of your business in a transition

By empowering management, you can prepare for your transition out of the business. A strong management team that can run the company in your absence opens up pathways for a successful transition.

A management buyout becomes a strong alternative to a retiring or passive owner, especially with a motivated executive team. Such an alternative can also serve as a retention strategy by minimizing risk to managers compared with a new owner while enticing key executives with ownership.

Sale of the company to an employee stock ownership plan (ESOP) can also reduce risk relative to a new owner. Additionally, it offers all employees the opportunity for ownership in the company while retaining the ability to competitively compensate key managers.

A strong management team increases the value of the company in the eyes of private equity buyers who are looking to back successful operators. If an owner can demonstrate to the private equity firm that the company can run without their presence, then this may give the owner the opportunity to exit completely from operational roles and possibly reduce any rollover investment into the company going forward.

A sale to a strategic buyer can give an owner a clean exit while offering management team members the opportunity to advance in a larger organization.

These planning exercises can help you empower your management team to become successful operators of the business. For more information, contact your advisor.

To manage big change, answer the critical questions

A while back, a prospective TravelNet Solutions client remarked that he would rather “take out his liver with a spoon” than change his PMS software again.

Maybe you can relate. Anyone who’s been in the hospitality industry a while probably has a horror story or three to share about a particularly disruptive and stressful software migration.

It goes something like this: We had a system, and maybe it didn’t work well, but it worked. We vetted all the vendors and made a decision that not everyone agreed with. Promises were made and expectations set. But implementation was a nightmare, training was inadequate, and everything broke. Our initial optimism gave way to despair, then anger, then a rare accord — that we must never change software again.

Sound familiar?

Why change a working system?

If it ain’t broke, don’t fix it. We all know the saying. The question of whether something is broken or not is a matter of fact. Whether it’s working as well as it could is speculative. The point being, nothing makes you second-guess a big change like a new tool that doesn’t immediately meet your expectations.

Even so, technology and competition pull us along, sometimes forcibly, toward change. And time after time, we hope for a dramatic improvement that requires very little from us, only to be disappointed that it’s not just our processes and systems that have to change. It’s us. The older we get, the harder that becomes.

Change happens in the gap between where we are and where we want to be. The smaller that gap, the harder it is to justify a disruption. Many hospitality pros are still enjoying their best revenue year ever, which makes that gap seem very small. But is it really?

The crucial question is whether strong performance came as a result of your current systems and processes or in spite of them.

When success is a red flag

A big revenue year is actually a perfect time to reflect. Some key questions to ask yourself:

To what extent did we create these results? If your performance was a direct or indirect result of a concerted effort, congratulations! You earned your success. Maybe you made capital improvements, ran some strong marketing campaigns, or hired additional staff. But if you can’t connect the dots between your results and your efforts, they should be taken with a grain of salt, which leads us to …

Are they repeatable? When market conditions favored or practically guaranteed success, as they did in 2021, ask yourself if it was an outlier or part of a stable trend. Sometimes a region just becomes a hot destination, in which case you may have entered a new normal. Look at the broader economic context for clues. If you had an up year, there’s a good chance everyone else did, too. If you grow without gaining market share, you probably left money on the table.

How did we scale? This is a big one. How did you manage the uptick? Did it make you feel overwhelmed and understaffed, or empowered? A busier than usual year tends to expose cracks in your operations that should be sealed before it happens again.

What does this success mean for us? If record revenues mainly helped you catch up, then you should look at how you got behind. Was it staffing? Expensive debt? Likewise, if you find yourself with more working capital than usual, maybe now’s the time to invest it.

When your software is holding you back

Most of our clients come to us not because systems and processes are broken, or even because they had a down year. It’s because they have a sense that they could or should be doing better. Maybe the system doesn’t do something you want, or your current vendor is ghosting you. There are lots of good reasons to gripe about software.

The sense of “wrongness” about your software can be a hard impulse to act upon because the numbers may not support it. If revenue is growing year over year and owners are happy, a gut feeling doesn’t seem like much to go on, especially considering how disruptive a software change can be. Still, if you know your market and think you ought to have a bigger slice of the pie, you’re probably right.

So how do you know if your hospitality software is holding you back?

Overwhelm.

If busy stretches leave you and your staff stressed and irritated, consider whether the tools you use all day, every day require too many steps or convoluted workarounds. Modern software such as Track uses triggers and automations to simplify routine tasks and seamless integrations that don’t require any heavy lifting from you. Even something that saves just ten minutes per day adds up to 40+ hours per year per person.

Proprietary technology. Hospitality is one of the last bastions of proprietary tech. Software built on the modern cloud is standards-based and device-agnostic, freeing you from old ecosystems designed to lock you in. If you have your own migration horror story, there’s a good chance proprietary software was involved.

Time since the last upgrade. If it’s been five-plus years since you overhauled your software, you’re probably missing out on a ton of cloud-based computing benefits that would help out your business, such as improved security, hassle-free updates, clean integrations, easy configurability, and of course, triggers and automations that work while you sleep. Hardware hasn’t changed all that much in the last several years, but software has seen some major shifts.

How many windows do people have open? If your staff immediately logs into ten or even twenty different systems to start their day, you’ve got a problem. Modern software like Track eliminates the need for “unitaskers” that ask too much of employees, especially sales agents. You’d be amazed how much a unified solution can do without requiring additional software.

High and/or fast turnover. The current hiring environment is hard enough without making new hires learn clunky software — especially if they’ve grown up with cloud computing. Dragging your employees back to 2010 is a quick way to lose them. If you’d describe your onboarding process as a “long ramp,” it might be time to modernize.

When to upgrade

There are two whens involved with an upgrade: When it becomes necessary, and when you should actually begin the process. Getting either of these wrong can lead to a poor experience, so let’s look at them in greater depth.

When is it time?

Not everyone is ready to change their PMS or CRM. If cash flow is shaky or you’ve just experienced some churn, like a managerial shakeup, you may want to wait until things have leveled out before upgrading. Nothing is more stressful than compounding changes.

Software is a major investment, so consider whether that money is already earmarked for something else. If you’ve already made a plan, it might be wise to stick to it and plan your upgrade for a later time.

It’s hard to know when it’s time to pull the trigger, but there are a few warning signs you shouldn’t ignore, all of which contribute to hidden costs:

It feels like you can’t afford to scale. If it doesn’t seem practical to grow without adding staff, it may be a sign that your systems and processes are already stretched to their limits. We have had more than one Property Manager who, before adopting Track, had made the difficult decision to stop bringing on new units because they felt their software was holding them back from scaling effectively.

Your system is like a game of whack-a-mole. Workarounds that “make” a system work for you add complexity, and complexity costs money.

High attrition, especially for new hires. If it’s hard to retain good employees in general, especially new hires, your system might be too hard to learn. Plus, when only a few key people know it well, they can feel put upon or simply leave and take that knowledge with them.

Chances are, any costs you identify as a result of operational problems and inefficiencies are just the tip of the iceberg. Software is no longer merely a tool. It has become the glue that holds hospitality operations together. There always comes a point when you can’t just squeeze another year out of your solution. Only you can know when that is.

When should it happen?

Not surprisingly, most migrations take place during the low season. But it’s not just your schedule you need to worry about. Software implementation teams are likely at their busiest when you’re at your slowest. That means striking a balance, which is why you should consider the shoulder seasons to implement. Regardless, we recommend initiating the process at least seven to nine months before you want to go live on new software. The right software transition will not be quick! If someone tells you can do this within a short period of time, run!

As with any complex project, planning ahead and pecking away at the prep work is the best way to avoid the hair-on-fire scenario that so many hospitality pros have come to associate with a software migration. Do yourself and your staff a favor and bake the prep work, such as auditing, into your regular activities — even when you’re busy “minding the store.”

How to manage a migration

Because a major software change is so important — and potentially disruptive — you should strongly consider appointing one person whose job it is to project-manage the process. This way, the time of year may not matter as much.

No matter how big or capable your shop is, nobody is going to think they have the time and expertise to take point on something like this. Clearing somebody’s plate is only going to put more stress on those who have to pick up their slack, and that’s a recipe for attrition.

One Track client created a technology coordinator position to manage not only the implementation itself but the vetting process as well, which took them well over a year. Evaluating vendors raises dozens, if not hundreds of questions and concerns that the vendor needs time to address. Having a single, dedicated point of contact simplifies matters for both you and the vendor, further minimizing potential disruptions or surprises when the time comes to flip the switch.

If you can’t hire a dedicated coordinator, know that something is going to have to give. Adding the job to somebody’s plate means their regular duties must change. Be ready to listen to their concerns, and be prepared to compromise.

Forming a committee

Ideally, you should also put a committee together to audit your current situation, clearly articulate your wants and needs, and make critical decisions with respect to the big change you’re planning to make.

The committee should comprise key stakeholders, including and especially people who are in your PMS, CRM, or call center software on a regular basis. It doesn’t have to be big, but it should include people in the front and back offices. Don’t fall into the trap of only having management at the table. In fact, the less management you have, the more honesty you might get. The thing they’re hesitant to mention might be the feature that unlocks your team’s full potential.

Let’s face it, the days of executives making big decisions alone are all but over. Shared governance is a fact of modern business. There’s too much at stake, and the people who hold the stakes need to be heard.

We cannot stress enough the importance of a functionally diverse committee in this decision-making process. Your people will spend more time in the software you’re buying than they will on Facebook or TikTok. They need to be part of the process, or you’ll invest in the wrong product.

Vet your vendors

If you’re under the impression that all solution providers will expertly shepherd you through the migration process, and that it mainly comes down to the software and the price, you might be in for an unpleasant surprise.

Software migration is fraught on both sides of the equation, no matter how sound the planning. You’re going to be on the phone, email, or chat a lot. Like, a lot. Things go awry. Key understandings are missed. You and your vendor are going to need each other, but you, the customer, will expect and deserve highly responsive service after the sale.

Ask your vendor about their support policies and tools. Ask about response times. Most importantly, ask what they spend each year on improving their migration experience and after-sale support. To date, TravelNet Solutions has invested more than $25 million in research and development. That’s part of a long-term growth strategy and not a short-term profits and consolidation strategy.

Finally, look carefully at the company leadership, structure, and funding. How experienced are they? What’s their posture toward innovation and customer feedback? What mechanisms are in place to build upon and improve their offering?

In Summary

Software migration horror stories abound, but such tales are slowly edging into myth. Standards-based software hosted in the modern cloud has taken a lot of the guesswork and hassle out of the implementation, but as noted earlier, problems can and will arise. Good software should adapt to you, not the other way around. Don’t settle for software that doesn’t have the flexibility to do what you need it to.

And definitely trust your gut when it comes to support. A capable, available, and responsive support team represents a huge investment that newer companies simply can’t afford to make. But without adequate support, even the best software can become practically useless.

Remember, a new vendor may have a deep understanding of your industry but know little or nothing about your particular operation and its quirks. The more involved they are in the end-to-end migration process, the better they will come to understand your specific needs and limitations, which is key to a smooth transition.

Change is hard, but it’s the only path to growth. Chances are, software migration has come a very, very long way since you last invested in new hospitality software. If you’re haunted by the ghosts of implementations past, take a closer look. Fear of disruption shouldn’t keep you from pushing your business to new heights.

If you have 50+ units under management and would like a free analysis and demo to see how Track could work for you, give us a shout. You’ll be glad you did.

As a progressive state with a population of less than 625,000, Vermont has long been a laboratory for lawmaking. Legislation in Vermont can serve as a pilot test for larger states with similar goals.

That trend has continued in its approach to regulating short-term rentals. Owning a vacation home in Vermont is a time-honored tradition built on the state’s picturesque beauty and appealing ski resorts. According to 2019 Census Bureau data, about 17% of Vermont’s total housing units are second homes.

Not all of those are rented out as vacation rentals. According to the Vermont Housing Finance Agency’s 2020 Housing Needs Assessment Report, short-term rentals make up 2.5% of the state’s total housing stock. The agency’s most recent tally (March) estimates there are about 8,300 short-term rentals across the state.

In the past two years, local and state officials have honed in on regulating vacation rentals. The regulations have largely been piecemealed from town to town, though Vermont does have some statewide rules in place.

Vermont currently has a statewide safety checklist for short-term rentals, which safety experts hail as the strongest of its kind. (The list, issued by the state fire marshal, goes beyond the quintessential smoke alarm to include GFI outlets, railing heights, stair railings, and other in-depth requirements, said Justin Ford of Breezeway.)

For two consecutive years, state lawmakers have also attempted to create the nation’s first statewide rental registry, which would include short-term rentals. Gov. Phil Scott vetoed the 2021 bill, Senate Bill 79. (Last year the legislature also considered House Bill 200, which would have disallowed out-of-state residents from renting their Vermont second homes as vacation rentals, but it did not pass.)

This year’s version, Senate Bill 210, looked as if it would meet the same fate – even though lawmakers weaved in provisions to exempt some short-term rentals from having to register.

Designed to increase the state’s limited housing stock, the program would provide up to $50,000 per unit to help homeowners renovate their properties or build accessory dwelling units. (Grant recipients would be prohibited from short-term renting buildings that receive this funding.)

The compromise bill also adds $400,000 to fund five full-time positions for a statewide safety inspection program to enhance safety at both long-term and short-term rentals.

Under the legislation, the state Division of Fire Safety would assume responsibility for rental property inspections from town health officers whose roles currently include responding to health and safety complaints at rental units.

Julie Marks, founder and director of the Vermont Short-Term Rental Alliance (VTSTRA), credits the slowing of both bills to the wave of engagement from short-term rental advocates.

“I think the massive public reaction that occurred after House Bill 200 was introduced had a big effect,” she said. She recounted being in the Statehouse in April and legislators still acknowledging how many emails they got in response to the bill.

Marks was at the Statehouse because she was one of a handful of people invited by a House committee to speak in person on Senate Bill 210. VTSTRA generally supports a registry with some modifications. For example, she cited the exemption for operators who rent less than 90 days a year as something the organization appreciated.

For those who rent more than 90 days per year, the legislation would have required homeowners to register their rental property annually with the Vermont Department of Housing and Community Development, pay an annual $35 registration fee, and provide detailed information about the rental unit.

Proponents of the registry say it would provide much-needed data about available housing in the state that could help inform how to invest tens of millions in federal housing dollars.

Several towns and cities in Vermont have already started registries for short-term rentals amid a groundswell of efforts to attempt to regulate the industry. The state bill would have consolidated that information into a statewide database.

The Vermont state legislative session runs through May. It is unclear if the statewide rental registry attempt will resurface again in 2023.

Local Perspective: Burlington

Burlington was one of the state’s first major municipalities to consider new rules. In response to the city’s housing shortage, Burlington City Council in February passed an ordinance that prohibited short-term rentals anywhere except inside permanent residences. The ordinance would have significantly reduced the number of short-term rentals in the city.

However, Burlington Mayor Miro Weinberger vetoed the ordinance in March, saying that it violated residents’ property rights.

“The City should not be interfering with the ability of residents to make personal decisions like this, and I am concerned that in doing so we will cause some residents serious hardship,” Weinberger wrote in a letter to city councilors.

He argued that the ordinance should allow property owners to add a separate short-term rental unit to their property such as an accessory dwelling, duplexes, or triplexes.

By levying a new fee or tax on short-term rentals, the city could generate income for building more affordable long-term housing through the city’s Housing Trust Fund.

City Council did not have the votes required to overturn the veto.

The successful end to the nearly two-year process was the result of the endurance and effort of dozens of people, said Marks, who was also a founding board member of the Burlington Short-Term Rental Host Coalition (now a chapter of VTSTRA). Advocates worked hard to form relationships with their council members and mayor and craft a unified message with solutions to their mutual goals.

“Having those two years to get to know the council, and to get to know each one has their own issues and agendas, we were able to tailor our conversations to each of them to collectively bring about an outcome that was desirable for us,” she said.

Still, Marks noted the legislative process is never over, and the end of every session means it is time to prepare for the next one.

In Burlington, their legislative “off season” was a quick one. Following local elections in early April, the newest cohort of council members began reworking the ordinance. A compromise ordinance by Councilor Sarah Carpenter addresses the mayor’s concerns while still slowing the growth of short-term rentals in the city.

The proposal would allow a short-term rental in accessory dwelling units, duplexes, and buildings with up to four units in addition to primary residences. If a host owns a multifamily building with one “affordable” long-term unit, they would be allowed to short-term rent a separate unit in the same building.

Councilors also were discussing adding a short-term rental fee that would help support the city’s Housing Trust Fund for affordable housing projects.

The councilors voted to have a committee review Carpenter’s proposal and report back with feedback and recommendations by June 1.

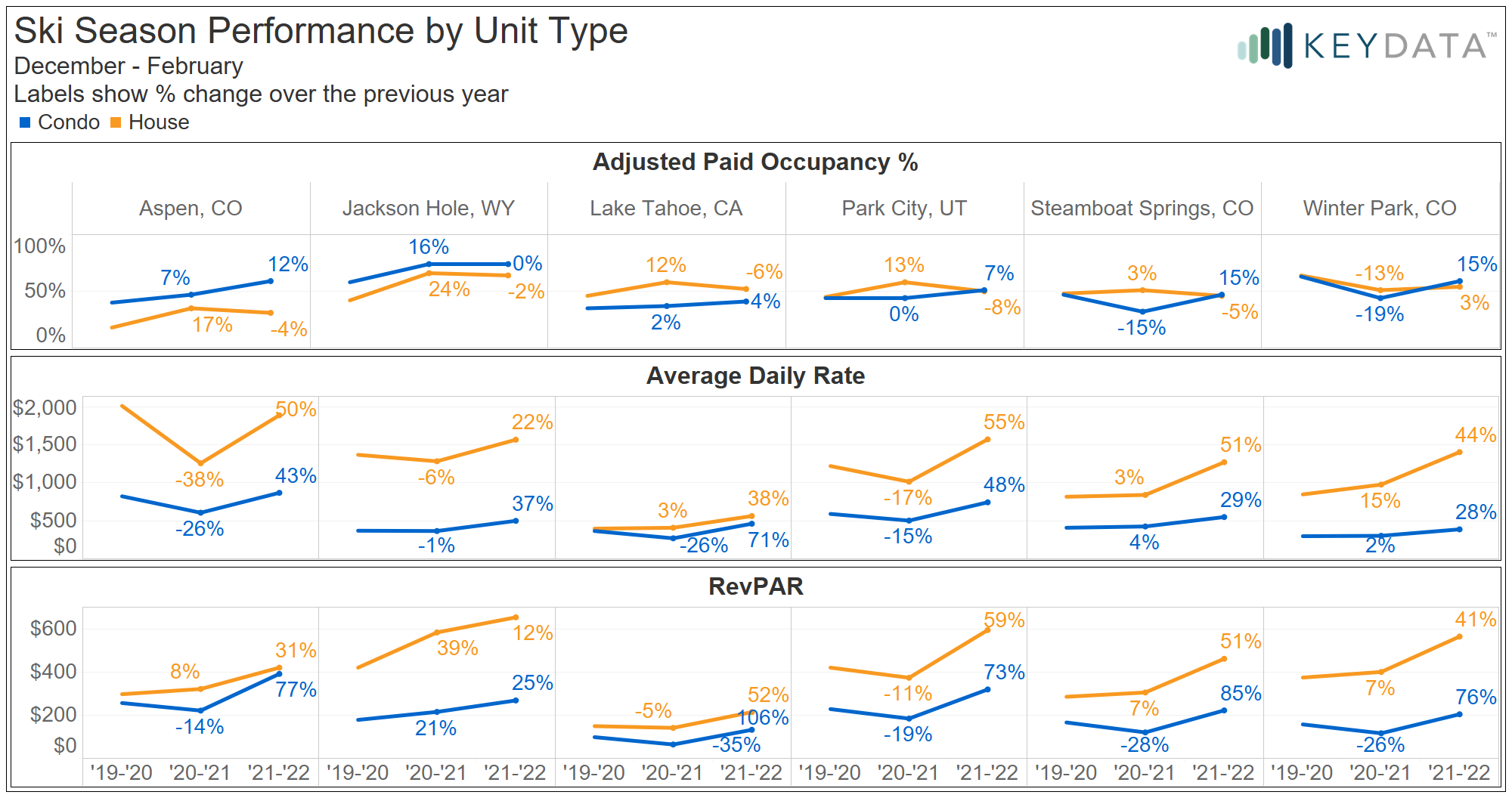

We’re taking the VRM Intel Live! Conference to the Ozark region for the first time next week to learn more about the area’s explosive growth in vacation rental activity. In Branson, alone, the number of vacation rentals catapulted from 2,002 homes in 2020 to 4,566 in 2022, according to AirDNA, with hundreds more new vacation homes in development. And Branson is not alone. The Broken Bow, Hot Springs, and Lake Ozark markets have doubled since April 2020, with average daily rates up over 30 percent across the region.

The conference, presented by Generali Global Assistance, will be held on Wednesday, May 18, at Chateau on the Lake in Branson, Missouri, and will bring together cabin rental companies, condo rental companies, short-term rental companies, real estate agents, investors, developers, and destination marketing organizations to discuss the latest information about the $13 billion vacation rental industry. Local speakers include Jonas Arjes, Jeramie Worley, Bill Dunton, Dan Boone, Valerie Budd, Cameron Jones, Micah Scott, and Cole Currier.

In 2022, vacation markets in the Ozarks, including Branson, are seeing some of the highest growth rates in the entire US. From Broken Bow and Hot Springs to Branson and Lake of the Ozarks, the entire Ozark region is seeing explosive growth in every category, including new construction. As a result, we’ve decided to host a regional event in the area to discuss professional vacation rental management, new technology advancements, recent development, and the data we’re seeing about future performance and booking activity.

The VRM Intel Live event will be an action-packed conference day filled with breakfast, lunch, workshops, classes, vendors, speakers, shopping, and networking. During this one-day event, we will discuss recent changes and key information for vacation rental success, such as opportunity zones, 1031 exchanges, tax benefits, performance data, regulations, technology, marketing, staffing, and insurance.

As stated by Mike Harrington, founder and CEO of Carolina Retreats, “If you can make it to a VRM Intel Live event as a professional in the vacation or short-term rental industry, do it.”

The one-day-only conference will take place at Chateau on the Lake, 415 N. State Hwy 265 Branson, MO 65616, on May 18, 2022, and feature over 30 speakers, including Jason Sprenkle, CEO of Key Data; Lino Maldonado, President of BeHome24; David Krauss, CEO of Rent Responsibly; Ben Edwards, CEO of Weatherby Consulting and Vacation Rental Management Association (VRMA) board member; the Branson Area Chamber of Commerice; and the Table Rock Lake Chamber of Commerce.

The cost to attend is $129, and you can use promo code OZARKS to receive 25 percent off. Tickets include access to all sessions, breakfast, lunch, networking breaks, and an end-of-day happy hour.

Delivering guest centric tools that lead to more direct bookings is a win-win for the vacation rental traveler and the dedicated hosts who serve them.

Stays Group, powered by Fetch My Guest, has teamed up with digital guest welcome book providers Touch Stay to enhance its commitment to guest experience excellence in the vacation rental community.

Digital guest welcome books adopted by Stays Group members close the loop on guest communications. Travelers supplied with their guest welcome book after booking confirmation will continue to experience Stays Group hospitality through pre-, during and post booking communications. They’ll also be able to explore the entire Stays Group portfolio, to consider future trips, from within each property’s guest guidebook.

“The Stays Group continues to grow our network of dedicated vacation rental professionals throughout North America. Part of our focus in 2022 is seeking out partnerships that complement the Stays Group network, our member brands and share our commitment to providing a world class guest experience. We are excited about this partnership with the Touch Stay team and look forward to expanding our relationship and many exciting announcements to come!” said Vince Perez, CEO of Fetch My Guest, Partner at Beach House Rentals, and Stays Group Member.

Andy McNulty, CEO of Touch Stay, adds: “Communication is perhaps the primary component of a guest’s experience once they’ve settled on where to stay. It’s our mission to enable it easily for hosts, owners and managers, and for it to be welcomed by and engaging for their guests. To work alongside partners who value and appreciate these endeavours is exciting for us and ultimately fulfilling for the sustainability and reputation of the vacation rental community.”

Photo: Waterfront homes in Surf City, NC, courtesy Gene Gallin

In 1994, the Conley family stepped onto their Emerald Isle vacation rental deck for a family photo. The deteriorated deck nails gave way under the weight of 20 people, and the deck collapsed, injuring several of them.

Jim Batten, then owner of Emerald Isle Realty (EIR), the property’s management company, lived just a quarter of a mile away. As soon as he heard what happened, he was immediately on the scene to see what he could do to help, said Julia Wax, his daughter and current owner of Emerald Isle Realty. “Of course, as a property manager, we have certain duties and responsibilities, but we also take it very seriously that we’re also their neighbor for that week.”

The Conleys sued Emerald Isle Realty, and the case made its way to the Supreme Court of North Carolina.

In early 1999, the court ruled in the property manager and homeowners’ favor, stating that the North Carolina Residential Rental Agreements Act that governs primary residence rental landlords does not apply to vacation rentals nor their brokers, thus applying the “buyer beware” principles of common law.

The decision created several new problems, questions – and opportunities – in its wake. Among them was the new risk that without the Residential Rental Agreements Act standards and the protection such regulations provide, vacation rental brokers were left vulnerable to other lawsuits and an absence of insurance providers willing to underwrite policies for short-term rental properties in the state. Furthermore, if vacation rentals were not considered residential, they could fall under more restrictive innkeeper laws governing hotels.

In the NC Supreme Court’s opinion, Chief Justice I. Beverly Lake Jr. closed with an encouragement of the state legislature to address what he called “a unique situation which does not appear to have been contemplated by our legislature.”

“Because our General Assembly has legislated so pervasively in the area of landlord-tenant relations, I join the majority in declining to make what I consider to be a badly needed change in this area of landlord-tenant liability,” he wrote. “This area of the law is ripe for legislative action.”

The Opportunities in Smart Regulation

And so it was. The vacation rental industry collectively recognized that in addition to safety and property care standards, there were three key challenges and headaches state legislation could help them solve.

Advance Payments and Property Sales

In the 1990s, properties were advertised primarily via catalogs. Property managers would send a printed book of their listings and weekly rates to prospective guests at the beginning of the year, who would then book their vacation months ahead and pay deposits to hold the dates.

Some property managers would disburse some or all of that income to the homeowners right away, leaving them in a bind should the guest cancel. They would pay the refund out of pocket and have to recoup the loss back from the homeowner. Some property managers would hold on to all or a portion of the advance payments to prevent this and would only disburse booking revenue to the owner once the guest checked in, but this created a competitive disadvantage in recruiting owners who wanted or needed their rental revenue right away.

Additionally, property managers had little to lean on when a property was sold. Property buyers could elect not to honor reservations on the books at the time of purchase, forcing the cancellation of guests’ reservations, sometimes on short notice with no availability to move them to comparable properties.

Evictions

Property managers also needed an enforcement solution for those who overstayed their lease. Long-term tenant evictions could take months, an option that would not work when a home’s next guests would be checking in within hours.

Evacuations

Finally, property managers needed a better way to handle mandatory evacuations. Particularly for managers on North Carolina’s hurricane-prone coast, they needed standards for handling refunds for guests who were forced to evacuate or who could not arrive at their vacation rental because of emergency orders or storm damage.

“We were just kind of lost,” said Tim Cafferty, owner of Outer Banks Blue and Sandbridge Blue. “There was nothing out there for us as vacation rental managers. We didn’t work under hotel-motel standards, and we didn’t fit under long-term rental standards.”

“The main thing was there was so much confusion, no rules and regulations in place that gave us in the industry anything to hang our hat on whenever a homeowner was upset or a guest was upset, and each company was doing the best they could to manage their company and their properties in such a way they could make a profit,” said Alan Holden, then owner of Alan Holden Realty and founding president of the North Carolina Vacation Rental Managers Association (NCVRMA). “It was just kind of like a bunch of wild horses running in different directions, or like a ship without an anchor; We needed something to hang our hat on and give us guidance.”

Coming Together

The state’s governing body over real estate sales and management, the North Carolina Real Estate Commission, took the lead in drafting legislation to fill the “unique situation.” Then Executive Director Phillip Fisher organized a task force of stakeholders from within the vacation rental industry and other important and influential voices to collaborate on a beneficial outcome.

Amongst the vacation rental industry representatives were Holden; Tim Midgett, owner of Midgett Realty and then chairman of the Outer Banks Tourism Board; the late Stewart Couch, then owner of Hatteras Realty; Doug Twiddy, owner of Twiddy & Company; the late S.R. “Buddy” Rudd, vice president with Margaret Rudd & Associates, Inc. and board member of the NCVRMA; and others. Several other property managers worked closely with task force participants in informal advisory roles, including Wax and Cafferty.

“It was the people in the industry who were the best practitioners who were very worried that they were in a situation where the law did not help them,” said Tom Miller, then special deputy attorney general, head of the real estate division. (At the time, the Real Estate Commission was a state agency within the attorney general’s office.)

Fisher brought in Miller, then Assistant Executive Director Miriam Baer, and Real Estate Commission General Counsel Blackwell Brogden to draft the legislation. He also invited David Kirkman and Harriet Worley from the state attorney general’s office, consumer protection division, to represent the interests of guests.

The group itself was not large, but each person represented an important perspective, Kirkman said, and there was a “desire on the part of several people to come up with a solution that didn’t harm the property owners or the consumers.”

The task force met – a lot, most interviewees emphasized. The stakeholders would come from all over the state to a big conference room at the Real Estate Commission and sit there all day, month after month, until they ironed it out, Miller said. He largely credits Fisher for creating “an environment for discussing policy where everybody was safe and people would eventually drop their defensiveness about their own constituencies and work together.”

“The great thing about a process like that is there’s no clock running, and by meeting over and over and over again, the representatives of these stakeholder groups got to know each other and trust each other,” Miller added. “And that’s how you make good legislation.”

Good Legislation

What they came up with was a robust but elegantly simple piece of legislation that solved everyone’s needs.