{kind=link}

With the 2026 FIFA World Cup schedule now public, early performance indicators across host markets are beginning to take shape. In a recent analysis released January 22, Key Data reports a mixed but instructive picture: guest check-ins remain uneven, yet pricing power is strengthening across most host cities.¹

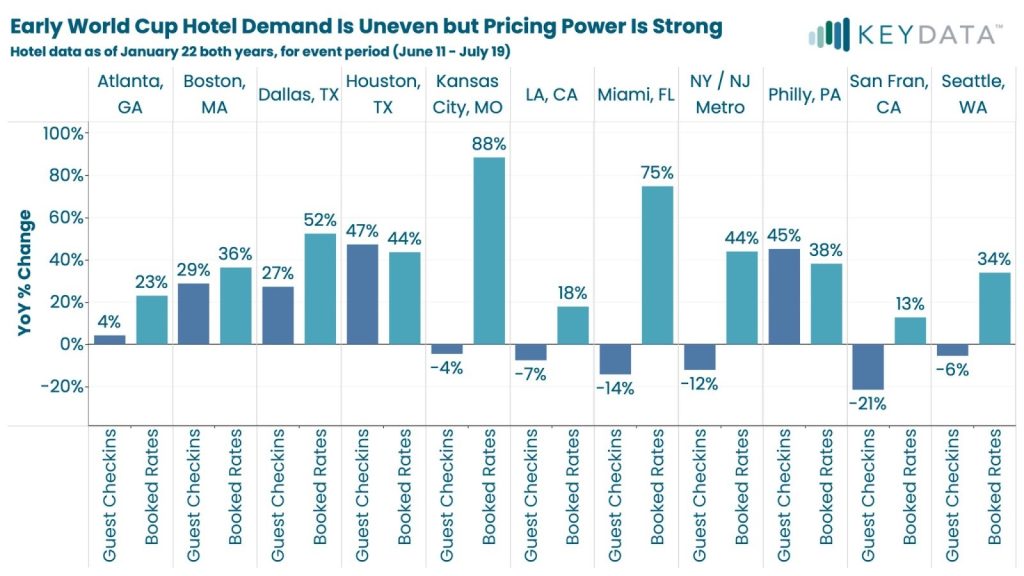

Year-over-year growth in check-ins varies widely. Houston leads with a 47 percent increase, while Boston approaches 29 percent and Dallas–Fort Worth posts roughly 27 percent growth. However, not all markets are pacing ahead. Kansas City, Los Angeles, Miami, New York/New Jersey, San Francisco, and Seattle show either minimal gains or negative early check-in comparisons.

Pricing, by contrast, tells a different story.

Booked rates across markets are up materially year over year. Dallas–Fort Worth leads with ADR growth exceeding 52 percent, followed by Miami at approximately 75 percent, Boston at 36 percent, and multiple additional markets posting increases between 30 and 45 percent. Even cities with softer early check-in growth are demonstrating rate strength.

The takeaway is clear: compression has not yet materialized, but operators are exercising pricing discipline early.

Demand Is Uneven — Compression Is Still Ahead

Occupancy for the event window remains below 7 percent across most markets, underscoring how far out bookings still are. The early pricing signals suggest confidence, but not yet volume.

Average lengths of stay between 2.5 and 3.2 nights align with match-driven travel patterns, reinforcing expectations of compressed, event-specific demand rather than extended stays.

This environment creates a delicate balance.

Early pricing momentum can tempt operators to either push rates aggressively or prematurely discount inventory to stimulate pickup. Yet the World Cup will likely unfold as a series of demand spikes tied to specific match clusters, not a single sustained surge.

Broader Implications for the Lodging Ecosystem

While the report centers on hotels, the uneven pacing highlights potential opportunity for adjacent accommodation types. Markets showing slower early pickup may see substitution effects later as match proximity increases and availability tightens.

For operators in host and drive markets, flexibility may prove more valuable than early aggression:

- Preserve inventory flexibility.

- Phase rate increases strategically.

- Monitor pickup patterns rather than headline ADR alone.

- Prepare for short, high-turnover stays rather than extended bookings.

Early pricing strength is encouraging, but the competitive landscape remains fluid.

The World Cup is not won in January pacing reports. It will be won in execution as compression builds.

For the full data breakdown and city-level analysis, see Key Data’s original release.¹

References

- Key Data, “Early World Cup Demand Is Here, but the Winners Haven’t Been Decided Yet,” January 22, 2026, https://www.keydatadashboard.com/blog/early-world-cup-demand-is-here-but-the-winners-havent-been-decided-yet.